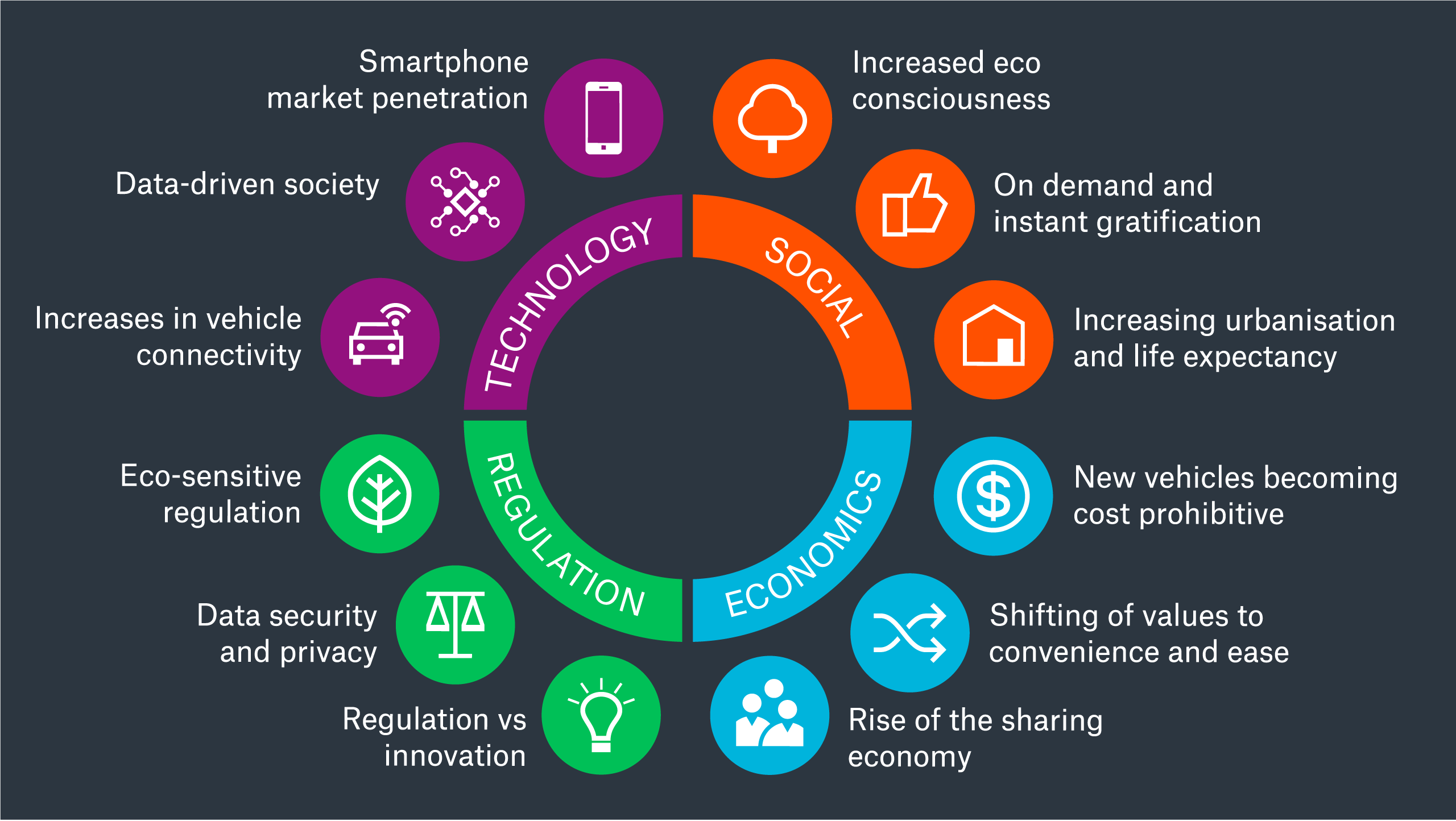

New mobility ecosystem

Preparing insurers and consumers along the entire value chain for the mobility of today and tomorrow.

properties.trackTitle

properties.trackSubtitle

New mobility insurance trends

| Connected usage-based insurance (UBI), pay as you drive (PAYD) | Mobility as a service | Technology-enabled fleets | Autonomous vehicles & advanced driver assistance systems (ADAS) | Electric vehicles |

|---|---|---|---|---|

| Challenges | ||||

| Capabilities for the processing of data generated through new sources Sensors, integrated in both vehicles and mobile phones, are moving into the mainstream, creating significant data. Do we have the right capabilities to capture, analyse and act on this new data for mobility insurance purposes? | Need for bespoke coverages Mobility as a service (MaaS) – from car sharing and rental to subscription or ride-hailing – is creating new needs with insightful data sets ... a new mobility ecosystem (is MaaS really the mobility ecosystem? – thin ADAS / Connected is included as well..) which requires new insurance and risk solutions. | Implications for profitability Commercial motor insurance is a growing market segment and a crucial line of business for many insurers. However, unprofitable combined ratios are commonplace. How does it correlate with technology-enabled fleets? | Impact on product, pricing and distribution The concept of the vehicle as the insured asset is changing radically through increased safety technology and connectivity. Do insurance solutions need to factor in how this impacts product, pricing and distribution? | How do the risks compare to internal combustion engines? Electric vehicles (EV) risk assessment and pricing is currently based on very limited data. The main topic mobility insurers need to address is: Do EV’s pose a higher, lower or comparable risk, relative to internal combustion engine vehicles? |

| Our offering | ||||

| Our solutions include strategic and operational consulting, products, pricing, analytics and technology via our own solutions and strategic partnerships. | MaaS platforms require unique products and services from insurers. We help our clients design flexible products that meet the needs of the market and mitigate risk through the use of increased data availability. | Vehicle technology can not only help make roads safer, but also improve profitability. We provide a modular consulting approach to our clients, primarily focusing on strategic guidance, underwriting and technology-based value proposition design. | We co-create approaches to jointly develop unique products and sophisticated pricing techniques for evolving vehicle technology. | We offer EV product consulting to set up dedicated EV coverages, and EV ratemaking by creating a full range of risk segmented features, tailored to the clients portfolio. |

Get in touch

Click any topic to explore further:

Connected mobility insurance

As the mobility behaviour of consumers changes through a more connected, shared and on demand transportation offering, privately-owned cars are becoming more connected and intelligent. Correspondingly, connected insurance and telematics solutions are undergoing significant growth. And the capacity to capture, store and analyse data, behavioural and mobility-related, generated from connected vehicles will be a key enabler in developing connected insurance products still further in the years ahead. Properly understanding the new risks inherent in connected mobility will permit higher profit per policy through risk-predictive behavioural scoring applied in the pricing process. It also will open up new touchpoints with customers, which will lead to higher brand stickiness and retention and, not least, significantly streamline the claims process.

Learn more about how we can work with you on connected mobility insurance solutions:

.jpg/_jcr_content/renditions/cropped.16_to_9.jpg./cropped.16_to_9.jpg "E-mobility")

Mobility as a service (MaaS)

New mobility platforms are driving a shift away from personally-owned modes of transport towards mobility solutions consumed as a service. Examples include:

- ride hailing,

- carpooling,

- subscription-based car ownership and

- micro mobility, such as electro scooters.

An insurance is fundamental to the business models of all of these new mobility platforms, be it for regulatory compliance, consumer trust or balance sheet protection. With this in mind, there is a pressing need for the insurance industry to design affordable, data-driven insurance products that enable MaaS providers to offer the necessary cover to their clients. In order to facilitate this process, insurers need a good understanding of new mobility business models, remembering that all new mobility segments represent risks that a large proportion of primary insurers would classify as non-core or edge-of-appetite for a number of reasons. These are the fluid nature of user behaviour, high vehicle utilisation, increased passenger exposure, unproven claims history, untested technology, and how the new models fit into existing infrastructure and social acceptance.

Learn more about how we can work with you on MaaS insurance solutions:

Technology-enabled fleet insurance

Insurers typically struggle to turn a profit on commercial auto. Their challenge is to price risks appropriately and limit balance sheet exposure. With this in mind, insurers need a way to help clients reduce risk exposure and lower costs. Leveraging data analytics and after-market safety technology to help reduce losses offers insurers the opportunity to create new data-driven commercial auto insurance products and services.

Our experience at Munich Re shows that, whilst getting the basics right in terms of risk selection, pricing and risk management remains fundamental. And using risk-mitigating technology helps elevate the traditional components of underwriting to new levels. By adopting a more data-driven approach and combining this with a redesign of the value proposition, insurers are not only able to carve out profitable market segments, but can also shift their motor fleet insurance offering away from a pure commodity purchase to a product that becomes integral to a client business.

Learn more about how we can work with you on technology-enabled fleet insurance solutions:

Insuring autonomous vehicles and advanced driver assistance systems

The implementation of advanced driver assistance systems (ADAS) and autonomous vehicle technology has significantly affected how we view risk, the result of which will be gradual replacement of traditional motor insurance with technology-based motor insurance. Within this new segment, the ability to capture, store, and analyse behavioural data, mobility patterns and vehicle data will be integral to how we underwrite and price mobility insurance. Solutions need to factor in all relevant new technologies, such as autonomous breaking or lane departure systems, and to consider their influence on the frequency and severity of vehicle accidents.

Autonomous vehicles

Globally, over 1.24 million people are killed each year as a result of collisions involving vehicles, not to mention the vast number of individuals and families affected by life-changing injuries suffered in road accidents. Our research indicates that around 80% of these accidents could be avoided with the predicted increase in automation. While there is no doubt that the potential societal benefits are immense, there are significant challenges for many industries as the road to automation develops, and the insurance industry is no different. Even though the decrease in accidents will undoubtedly reduce the need for motor third-party liability covers, or at least lead to a reduction in premiums, insurers also need to consider a potential shift in dependency from retail to commercial risks.

In particular, as autonomous vehicle technology becomes more widespread it is likely to result in a shift in consumer behaviour towards mobility consumption rather than car ownership. As a result, we may see a shift from retail to commercial dependence. Insurers with retail-dominated portfolios may need to review their business models in order to remain relevant in the future.

Learn more about how we can work with you on insuring autonomous vehicles and ADAS:

Mobility insurance for electric vehicles

The distribution and registration of electric vehicles worldwide hits new records every year. For example, over 10 million electric vehicles (battery electric vehicles and plug-in hybrid electric vehicles) were sold globally as at the end of 2020, an increase of almost 3 million over the previous year.

A number of factors are stimulating demand for e-mobility. These include government incentive schemes, expanding new vehicle charging ecosystems, decreasing manufacturing costs of high-voltage batteries, EV’s drawing closer to internal combustion engine vehicles in terms of cost, and a growing number of EV models being produced by OEM’s (see diagram below). These trends will only accelerate, making refinement of EV risk assessment all the more urgent. Rising EV sales are both an opportunity and a hard-to-quantify risk for motor insurers. The fact that it is a relatively new market means that there is currently insufficient data available to properly price EV solutions. It is not yet known whether electric vehicles pose a higher, lower or similar risk when compared to internal combustion engine vehicles.

Learn more about how we can work with you on EV solutions:

41 %

Your challenges at a glance

Usage-based insurance

New mobility platforms

Electric vehicles

Forecast of worldwide market volume of autonomous driving functions

Advances driver assistance systems (ADAS) and autonomous vehicles

This leads us to the projection that traditional motor insurance will gradually be replaced by technology-based motor insurance, we also call it smart risk taking opportunity.

Within this new segment the ability to capture, store, and analyse behavioural data, mobility pattern, as well as vehicle data will become an integral part to appropriately underwrite, price and drive value for customers.

94% of vehicle crashes are due to human error. 80% of these crashes may be reduces or eliminated by automation.

Advanced driver assistance systems (ADAS)

ADAS systems as an important step towards autonomous transportation.

Advanced driver assistance systems, with such safety features as autonomous breaking or lane departure systems, are increasingly being built into today’s cars. This is an important step for increasing safety on our roads and towards the journey of fully autonomous transportation.

The bigger question is how do ADAS influence the frequency and severity of accidents? And how can the insurance industry take this trend into account when building pricing tariffs and risk models? It is a challenging task for insurers to understand what safety features are built into which cars, how they act across different manufacturers and if they are actively being used by the insured.

Munich Re has been researching and developing across this field for many years and has a acquired extensive knowledge on the effectiveness of ADAS features. We support our clients globally to understand their portfolio composition, the penetration of ADAS features within their book of business as well as by analysing the impact on risk.

Mobility platforms

New mobility platforms are the fuel for changing consumer behaviour and evolving how we move from from point A to B. Ride hailing, carpooling, subscription-based car ownership and micro mobility such as electro scooters, for example, require not just new insurance products but also the development of new strategic partnerships and alliances.

While insurance may not have been at the forefront of many founder’s minds in the early days, it is now fundamental to the business models of all new mobility platforms, be it for regulatory compliance, consumer trust or balance sheet protection.

Understanding the business model

It is important for insurers to really understand the business model of these new players in order to influence appropriate product designs and services. If we take ride sharing as an example, there are three distinct client groups within each journey: the platform itself, the driver and the passenger. Insurers have the opportunity to deliver products and services to each of these groups, whether it be corporate coverage at platform level, dynamic motor coverage for drivers or experience enhancements for passengers.

Risks & opportunities

There is no doubt that the new mobility sector represents a massive opportunity for insurers.

These segments represent risks that a large proportion of primary insurers would classify as non-core or edge of appetite for a number of reasons: the fluid nature of the users, urban locations, high vehicle utilisation, increased passenger exposure, unproven claims history, untested technology as well as how the new models fit in to existing infrastructure and social acceptance.

What can we do to mitigate?

At Munich Re we understand these risks and have a proven track record of creating innovative products and services that deliver value. We have the opportunity to utilise vast amounts of data like never before to establish new underwriting methodologies, sophisticated product design and acceptance criteria as well as real time incentivisation in order to deliver products that really add value to customers. Consumers have the opportunity to make a profitable contribution to insurer portfolios as well.

Connected & usage-based insurance (UBI)

Connected insurance is becoming mainstream. In 2018, we reached 24.3m UBI policies (+47% yoy) with 403 programmes in 54 different countries. However, only two markets globally reached an insurance penetration above 10%: Italy, the pioneer of using telemetry data for fraud (17%) and South Africa, with a strong use case on theft (10%). The smartphone as a sensor is now transforming connectivity even further. Via apps we can now turn our mobile phones into powerful connected car devices. This significantly reduces costs and complexity while increasing the overall customer experience.

The mobility behaviour of consumers is changing through a more connected, shared and on demand transportation offering. Yet, privately owned cars are becoming more connected and intelligent as well. This requires the insurance industry to adapt and develop insurance products that fit the needs of the customers of tomorrow. The ability to capture, store and analyse behavioural, mobility and data generated from the connected car will be a key competence. This will serve as an enabler to build connected insurance products going forward. Usage-based insurance is a first step in this direction.

We have built extensive knowledge and thought leadership within our Global Consulting team and developed a set of hands-on services that help accelerate the journey of our clients towards a connected, data-driven and digital insurance product factory.

Autonomous vehicles

There are many societal benefits and positive arguments for vehicle automation. Over 1.24 million people are killed each year as a result of road collisions, not to mention the vast number of individuals and families affected by life changing injuries suffered in road accidents.

While it is difficult to put an exact number on how many of these collisions could have been avoided, our research shows that 94% of crashes can be attributed to human error, we believe that around 80% of these accidents could be avoided with the predicted increase in automation. That equates to just under 1m lives saved each year as a result of autonomous vehicles.

While there is no doubt that the potential societal benefits are immense, there are significant challenges for many industries as the road to automation develops – the insurance industry is no different.

We believe, that these 3 key areas w will impact the take up rates of autonomous vehicles:

People:

- Public acceptance

- Giving up total control

- Data privacy issues

- Cyber-attack concernes

Infrastucture:

- Receptive infrastructure needed to allow optimal functionality

- Costs

- Territorial limitations

Vehicles:

- Long transition periods

- Mixed traffic

What does this mean for the insurance industry?

We have reviewed 6 key coverages and predicted how these may be impacted by the rise of automation:

- Auto liability - likely to shrink

- Cyber risk/IoT – likely to increase

- Product liability – likely to increase

- Auto physical damage – no material change

- Equipment breakdown/Warranty – likely to increase

- Product recall – likely to increase

Portfolio rebalancing

Even though the reduction in accidents will undoubtedly reduce the need for MTPL covers, or at least a reduction in premiums, insurers also need to consider a potential shift in dependency from retail to commercial risks.

We project that as autonomous vehicle technology becomes more widespread, coinciding with the rise of mobility platforms, this will result in a shift in consumer behaviour towards mobility consumption rather than car ownership. As a result, we may see a shift from retail to commercial dependence. Insurers with retail-dominated portfolios may need to review their business models in order to remain relevant in the future.

How is Munich Re dealing with the rise of autonomous vehicles?

- Presently covering autonomous vehicles across multiple territories

- Cooperation with automotive suppliers

- Partnering with AV start-ups to vitalize progress

- Cooperation regarding data classification and analysis

- Participation in nationwide working groups on future mobility and new mobility concepts

- Development of best practices for safety guards

Electric vehicles

Distribution and registration of electric vehicles worldwide are hitting new records year to year. In many markets, electric vehicles and their associated infrastructure are still benefitting from government backed incentive schemes. However a gradual shift from traditional combustion engine to green or zero emission vehicles is undeniable.

One dominant issue is the question of whether electric vehicles are posing a higher, lower or comparable risk, when directly compared to typical vehicles relying on combustion engines.

We have analysed the most prominent factors and predicted how these will impact the risk presented by EVs:

- Range anxiety & lack of infrastructure: May lead to an increase in urban use in the short-term. However, as battery technology improves and infrastructure investment increases we may well see policyholder geographical distribution return to normal.

- Lack of engine noise: Approaching electric vehicles are not perceived in time by other road users, especially pedestrians, children & cyclists. However, some manufacturers have installed simulated engine noise to mitigate this risk.

- High torque potential: This feature in an electric vehicle could entice drivers interested in a sporty driving style.

- Repair costs and supply chain issues: Technology of electric vehicles (e.g., components, battery packs, high-voltage components and charging interfaces) complicates repairs of damaged vehicles and leads to increased repair costs and timelines.

- Risk of electric shock: In particular after a vehicle crash for drivers, passengers and third parties (police, ambulance, rescue teams and helping hands).

- Cyber risk: Electric vehicles are often highly innovative vehicles. This could result in higher cyber and software risk to electric vehicles (hacking, illegal engine tuning, faulty updates, etc.).

- Charging equipment: Components could be subject to additional and new risk scenarios such as stumbling over cables in public by third parties.

- Hazardous substances: Chemical materials from a leaking or damaged battery could cause severe environmental pollution.

Our solutions

Innovative solutions

Industry solutions

Contact our experts